Global scenario and implications for Latam

The global scenario remains positive for Latam, even considering the recent escalation of the conflict between the U.S. and Iran. Regarding U.S. economy, although GDP growth for the fourth quarter of 2025 surprised to the downside—mainly due to the government shutdown during the quarter—expectations for 2026 have been revised upward and remain above potential, supported by fiscal stimulus effects on consumption and investment, the transmission of last year’s interest rate cuts, continued AI‑related capex, and stronger productivity expectations. As a result, the economy continues to avoid recession despite pressures from higher tariffs. However, the conflict between U.S. and Iran increases the near-term risk of additional inflationary pressures linked to energy prices.

The labor market remains crucial to this outlook. Job creation continues to slow in February, driven by temporary factors such as severe weather, and strikes in the healthcare sector. At the same time, more structural patterns continue to show their impact, including demographic shifts, reduced immigration, government budget cuts, and advancements in AI. Nevertheless, the rise in the unemployment rate was limited, and wages grew at a better-than-expected pace, indicating that the labor market remains in a state of low hiring and low layoffs. The second key factor is inflation, which is likely to remain above target in 2026. During the first half of the year, inflation pressures will persist due to tariff pass-through, but headline inflation is likely to gradually ease in the second half as other disinflationary forces—such as softer housing prices and slower wage growth—take hold, reducing the risk of a wage‑driven rebound. However, recent geopolitical tensions have put pressure on inflation expectations given the recent spike in oil prices due to the Middle East War. In this context, the Fed is expected to maintain a very cautious and data‑dependent stance. Additional rate cuts may only materialize in the second half of 2026 and only if the energy price pass-through is limited and the conflict proves short-lived. Overall, a scenario where the Fed still has room to cut rates is positive for emerging markets.

For Latam, despite higher tariffs and higher energy prices, trade patterns remain stable and growth resilient, as most countries are net oil exporters. If the conflict in the Middle East is short-lived, the dollar could resume its downward trend which, together with slowing inflation in the region, would give central banks more room to cut interest rates, especially in Brazil and Mexico. Finally, even with limited tariff impact and prospects of lower rates, upcoming local elections could increase volatility in the region, especially amid elevated geopolitical risks.

Brazil

Economic Activity

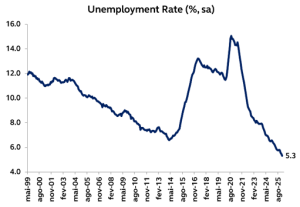

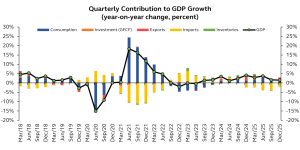

On the economic front, attention remains focused on the pace of activity deceleration and its implications for monetary policy. The fourth-quarter GDP release reinforces the ongoing slowdown, with growth of just 0.1% quarter-over-quarter, marking a second consecutive quarter of near-stagnation. As a result, GDP growth reached 2.3% in 2025.

Source: IBGE, FGV and Principal Asset Management

Source: IBGE, FGV and Principal Asset Management

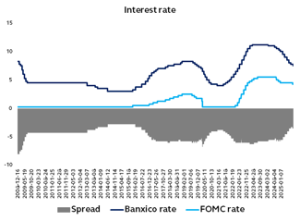

Inflation and Monetary Policy

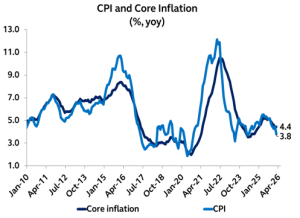

On the inflation front, recent developments have been somewhat unfavorable at the margin, but without changing the broader disinflationary trend observed in recent months. After a prolonged sequence of downside surprises, the February IPCA-15 came in above market expectations, rising 0.84% month-over-month. However, most of the upside surprise was concentrated in more volatile components, such as airfares, while underlying inflation measures remained more contained. More importantly, the recent print does not materially alter the ongoing process of inflation convergence, particularly when considering measures of core inflation and services, which have shown signs of gradual moderation. On a year-over-year basis, headline inflation slowed from 4.5% to 4.1% in February.

Looking ahead, the inflation outlook remains broadly consistent with a gradual disinflation process, although risks remain asymmetrically tilted to the upside in the short term. These risks stem from still-resilient domestic demand, potential second-round effects from recent cost shocks

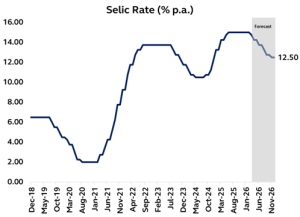

Against this backdrop, the combination of a gradual slowdown in activity and a still relatively benign inflation environment allows the Central Bank to begin the monetary easing cycle at the upcoming meeting. However, the presence of upside risks to activity in the first quarter as well as uncertainties related to geopolitical developments and their potential spillovers to the domestic economy, are likely to keep the Central Bank cautious, particularly at the early stages of the easing cycle.

Source: IBGE and Principal Asset Management

Source: IBGE and Principal Asset Management

Fiscal accounts and political scenario

On the fiscal front, the 2025 fiscal deficit ended the year within the target set by the fiscal framework. However, attention is shifting to 2026, an election year in which additional fiscal stimulus measures may be deployed. Moreover, medium-term challenges to fiscal sustainability further underscore the importance of the electoral debate and the definition of a more sustainable economic policy over the longer term.

On the political front, attention is increasingly turning to the 2026 elections. Although still relatively distant, the potential for a change in power is making the topic progressively more relevant for markets. On the government side, the overall assessment of the current administration remains negative. Disapproval ratings continue to stand at historically elevated levels for the Lula administration, and the more favorable economic backdrop, with moderating inflation and a strong labor market, has not yet proven sufficient to reverse this trend.

On the right, Flávio Bolsonaro’s candidacy has gained traction following recent improvements in polling, keeping him as a relevant contender in the presidential race and reinforcing uncertainty around the electoral outcome. This does not necessarily rule out the possibility of a change in power, but it does point to a more turbulent path toward the election.

Chile

Economic Activity

Chile’s GDP grew 1.6% yoy in 4Q25, taking full-year growth to 2.5%, slightly above the Central Bank’s latest 2.4% estimate. The result points to an economy that performed somewhat better than expected, especially as it was also accompanied by upward revisions to 2023 and 2024 growth.

The composition of growth was more encouraging than in previous quarters. Domestic demand led the expansion, with both consumption and investment showing a clearer recovery, while investment stood out as the main growth driver during the year. By contrast, the external sector was less supportive, as stronger imports offset part of the improvement in exports.

At the sector level, performance remained uneven. Commerce, manufacturing, and services posted the strongest gains, while mining and utilities lagged behind. Overall, the data suggest Chile ended 2025 on a somewhat firmer footing, supported mainly by stronger domestic demand and a rebound in investment.

Source: Central Bank of Chile

Inflation and Monetary Policy

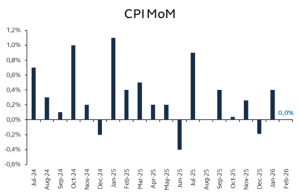

February CPI was flat on the month, bringing annual inflation down from 2.8% to 2.4%, below the 0.1% monthly increase expected by the market. Core measures were also contained: CPI excluding volatile items rose 0.2% m/m, while CPI excluding food and energy increased 0.1% m/m, leaving their annual rates at 3.3% and 2.5%, respectively. Inflation breadth also eased meaningfully, with the share of items posting monthly price increases falling to 52.7% from 60.8% in January.

Even though February’s 0.0% monthly print points to a still-benign inflation backdrop, the recent rise in oil prices and the risk of further pass-through into domestic prices remain important sources of uncertainty. That should keep the Central Bank cautious, as any renewed inflationary pressure could complicate the path for additional policy easing.

Source: Instituto Nacional de Estadísticas (INE)

Source: Instituto Nacional de Estadísticas (INE)

Fiscal accounts and political scenario

Since taking office, President Kast has moved quickly to deliver on key campaign promises, particularly on investment, deregulation and the reduction of bureaucratic hurdles. The new administration has already launched a National Reconstruction Plan focused on tax certainty, faster project approvals and permit reform, explicitly targeting the bureaucracy that has long delayed private investment. A tax bill expected in April would lower the corporate tax rate from 27% to 23% and introduce other pro-growth measures, reinforcing an early business-friendly signal.

Kast has also paired that agenda with a broad fiscal adjustment plan, including nearly US$4 billion in spending cuts for 2026, underscoring a strong emphasis on execution, discipline and speed in the administration’s first days. This has reinforced the perception that the new government is moving rapidly to translate campaign rhetoric into concrete policy action, especially on growth, investment and the state’s role in facilitating rather than obstructing projects.

Still, expectations surrounding Kast’s presidency remain high, which also raises the bar for delivery. The key challenge now is whether this early momentum can be converted into visible improvements in investment, activity and confidence over the coming quarters.

Mexico

Economic Activity

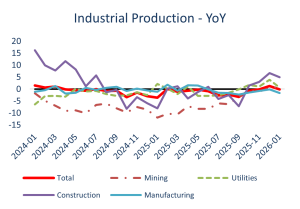

Activity entered 2026 on a softer footing following the stronger-than-expected close to 2025, with January data showing mixed signals. Industrial production declined 1.1% MoM and slowed to 0.1% YoY (from 1.3% previously), reflecting broad-based weakness across sectors. Manufacturing contracted 1.1% MoM despite improving annual growth (1.7% YoY vs. -0.1% in December), with declines in key segments such as transport equipment and electronic components. Construction also took a breather (-1.1% MoM), following a strong 4Q25, with annual growth moderating to 5.0% YoY. Overall, the start of the year points to a temporary loss of momentum rather than a reversal of the recovery trend. Despite the weak January print, the outlook remains constructive. Domestic demand fundamentals are broadly unchanged, with consumption still supported by resilient labor market conditions and real wage gains, while investment should strengthen as public spending accelerates. The decline in construction appears transitory, as the higher expenditure budget for 2026 has yet to materialize, and additional mixed-investment projects equivalent to nearly 2% of GDP should provide a meaningful boost.

Externally, rising geopolitical tensions—particularly the conflict in Iran—pose new risks, though the overall impact on Mexico should remain contained under a temporary shock scenario. Higher oil prices are now neutral to slightly negative for growth, as Mexico’s position as a net oil importer implies a deterioration in the energy trade balance. While fuel subsidies help cushion the pass-through to inflation, they increase fiscal pressures and reinforce external headwinds. Even so, Mexico’s is relatively well positioned to absorb the geopolitical shock given solid external accounts, institutional credibility, a strong MXN and manageable fiscal accounts.

Source: INEGI and IMSS

Source: INEGI and IMSS

Inflation and Monetary Policy

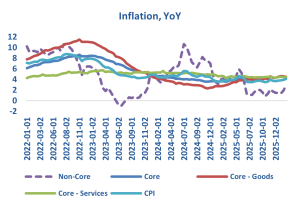

Inflation data in February delivered a more concerning signal, interrupting the relatively benign start to the year. Headline CPI rose 0.50% MoM—slightly above expectations—and accelerated to 4.02% YoY (from 3.79% in January), breaching Banxico’s upper bound for the first time since mid-2025. The increase was largely driven by a sharp rebound in agricultural prices, particularly fruits and vegetables, lifting non-core inflation. However, underlying dynamics remain challenging: core inflation rose 0.46% MoM and remained elevated at 4.50% YoY, with persistent pressures in services and early signs of normalization in core goods. While the composition showed some mixed signals, the data reinforces the view that disinflation remains gradual and subject to renewed volatility.

Looking ahead, the inflation outlook remains broadly unchanged, but risks are increasingly skewed to the upside. External factors—notably higher oil prices linked to geopolitical tensions—pose an important upside risk, given Mexico’s sensitivity to gasoline prices within the CPI basket. While potential fuel subsidies could partially mitigate the pass-through, a sustained increase in oil prices would still exert upward pressure on headline inflation. At the same time, domestic drivers—including sticky services inflation and a faster-than-expected rebound in non-core components—suggest that underlying pressures may prove more persistent than previously anticipated.

Against this backdrop, Banxico is likely to maintain a cautious easing stance. While we cannot rule out a 25bp rate cut in March since the Board is poised to deliver additional easing, the window for cuts is narrowing. Higher headline inflation, combined with the risk of a longer than anticipated conflict in the Middle-East and peso depreciation under tighter global financial conditions, could delay or even pause the easing cycle. Overall, inflation dynamics reinforce a scenario of gradual convergence with heightened sensitivity to external shocks, keeping monetary policy firmly data-dependent.

Source: INEGI and Banxico

Source: INEGI and Banxico

Fiscal policy and political scenario

Fiscal policy remain stable but is closely tied to developments in energy markets. As a net oil importer, rising refined product imports—particularly gasoline—continue to offset crude export gains, implying a deterioration in the oil trade balance. While oil exports still provide an important revenue stream, declining production and structurally strong domestic fuel demand limit the upside from higher prices. In this context, fuel subsidies play a central role: they help cushion the pass-through to consumers and contain inflationary pressures, but at the cost of higher fiscal burdens and a weaker external position.

From a fiscal standpoint, the overall impact is slightly positive but constrained. Higher oil prices boost Pemex revenues and, by extension, government oil-related income; however, this benefit is largely offset by the rising cost of gasoline imports (around 2/3 of total consumption). The recent decision by the Ministry of Finance to reduce excise taxes—and potentially reintroduce subsidies to cap gasoline prices—highlights this trade-off. While such measures support household purchasing power and short-term stability, they also limit the fiscal gains from higher oil prices.

All else equal, this dynamic represents a mild headwind for the peso, although Mexico’s institutional credibility and policy framework should continue to support relative resilience.

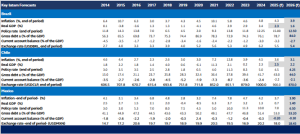

Key Latam Forecasts

Autores

Marcela Heilbuth Pereira Rocha- – Chief Economist – Brazil at Principal Asset Management

Carlos Bautista – Sr. Research Manager LATAM

Ramiro Torres – Research & Quantitative Analysis Assistant Manager

Aviso Legal

This material covers general information only and does not take account of any investor’s investment objectives or financial situation and should not be construed as specific investment advice, a recommendation, or be relied on in any way as a guarantee, promise, forecast or prediction of future events regarding an investment or the markets in general. This report has been prepared for informational purposes only. It is neither intended, nor should be considered, as an offer, solicitation or recommendation to buy or sell shares of any investment fund managed or sponsored by any entity of Principal Asset Management Ltda. nor should it be construed as such in any jurisdiction where such offer, solicitation or recommendation would be illegal. This presentation is not intended to be, nor should be considered, a basis for any contract for sale or purchase of any security, loan or other financial product, or as an official confirmation, or statement of Principal Asset Management. Unless otherwise noted, the information in this document has been derived from sources believed to be accurate as of April 2025. Principal Asset Management is a trade name of Principal Global Investors, LLC, a member of Principal Financial Group. Principal Asset Management Ltda. is a Brazilian asset manager licensed and authorized to carry out its activities in Brazil according to Declaratory Act n. 9.408/07.